SMM Alumina Morning Comment on June 11

Futures Market: Overnight, the most-traded alumina 2509 futures contract opened at 2,887 yuan/mt, with a high of 2,897 yuan/mt, a low of 2,870 yuan/mt, and closed at 2,870 yuan/mt, up 2 yuan/mt or 0.07%, with open interest at 304,000 lots.

Ore: As of June 10, the SMM imported bauxite index was reported at $75.12/mt, unchanged from the previous trading day; the SMM Guinea bauxite CIF average price was reported at $75/mt, unchanged from the previous trading day; the SMM Australian low-temperature bauxite CIF average price was reported at $70/mt, unchanged from the previous trading day; the SMM Australian high-temperature bauxite CIF average price was reported at $65/mt, unchanged from the previous trading day.

Basis Report: According to SMM data, on June 10, the SMM alumina index had a premium of 356.38 yuan/mt against the latest transaction price of the most-traded contract at 11:30.

Warrant Report: On June 10, the total registered alumina warrants decreased by 3,299 mt from the previous trading day to 87,100 mt. The total registered alumina warrants in Shandong remained unchanged from the previous trading day at 601 mt, in Henan at 300 mt, in Guangxi at 3,001 mt, and in Gansu at 0 mt. The total registered alumina warrants in Xinjiang decreased by 3,299 mt from the previous trading day to 83,200 mt.

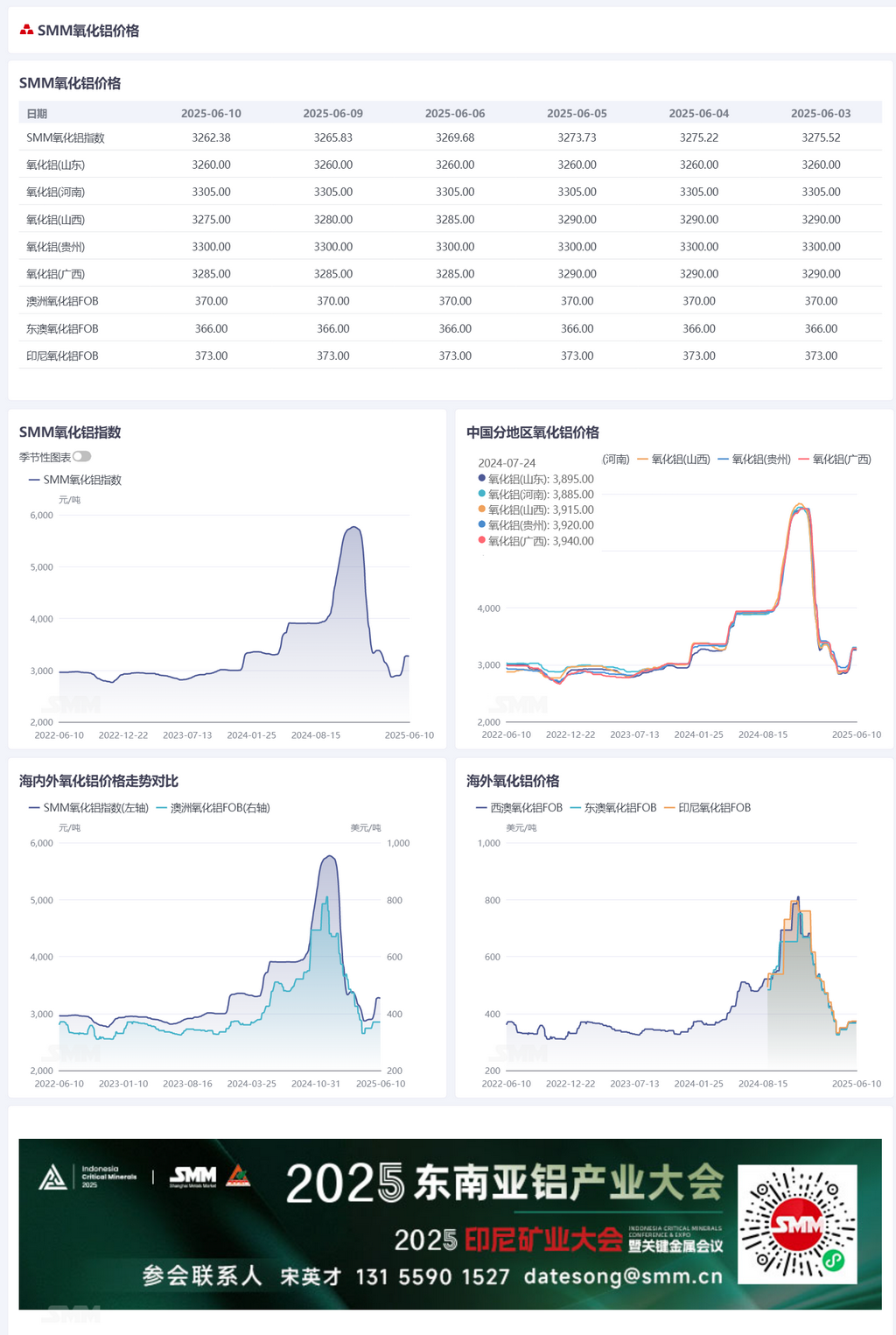

Overseas Market: As of June 10, 2025, the FOB Western Australia alumina price was $370/mt, with an ocean freight rate of $21.85/mt. The USD/CNY selling rate was around 7.20. This price translates to an external selling price of approximately 3,270 yuan/mt at major domestic ports, which is 7.26 yuan/mt higher than the domestic alumina price. The alumina import window remained closed.

Summary:

Last week, the operating capacity of alumina increased by 600,000 mt/year to 87.27 million mt/year. It is understood that some imported alumina arrived at Chinese ports. Supply improved while demand did not change significantly. Last week, the total inventory of alumina at aluminum smelters increased by 19,000 mt to 2.63 million mt. As of June 10, imported alumina prices were still incurring losses, and the import window remained closed. In the short term, the alumina fundamentals are expected to remain relatively loose, with spot alumina prices likely to be in the doldrums. Subsequent attention should be paid to changes in the capacity of domestic alumina enterprises and the transportation of previously imported alumina.

[The information provided is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make cautious decisions and should not rely on this as a substitute for independent judgment. Any decisions made by clients are not related to SMM.]